How a Tiny British Startup Became Silicon Valley's Hottest Acquisition

Tiny British startup? Hottest? How?

I said “oh shit” a few times this week.

First, on Wednesday, when a 62-year-old Tom Cruise stepped out of a helicopter at fifteen thousand feet, torched his parachute mid-spin, twisted through a plume of burning nylon, and landed with every hair in place.

Bravo.

The second came when Hims announced it was buying Zava. That deal is the centrepiece of this week’s GLP-1 Digest, and I have a contrarian take I’d like to share with you.

Before we dive in, a quick thank-you. The growth of this newsletter has surprised me, in the best way. Your attention is a vote of confidence I don’t take lightly.

On that note, time to strap in.

Everyone is calling the Zava acquisition a growth move. I see it as a defensive play — Word on the street says Hims paid roughly £100-300 million for a business that made only £20 million in sales in 2023. Even at £50m following the post GLP-1 boom, the revenue is tiny in a market where rivals post nine-figure quarters.

No, I don’t think revenue is the prize here.

The real payoff is unlocking four tricky markets in one go. Zava reaches about 1.3 million cash-pay users spread across the UK, Germany, France, and Ireland.

More importantly, they’ve got their hands on that sweet, sweet EU paperwork: pharmacy licences, local prescriber panels, GDPR proof data infrastructure, and advertising playbooks that ‘dodge’ each country’s ban on promoting prescription only medications to the public.

Because Zava has already cleared this nightmare-ish bureaucratic maze, Hims can launch across the EU without the years of regulatory groundwork. In Germany alone, getting approval for a new digital health platform typically takes 18-24 months. In France, navigating the ‘Assurance Maladie’ system while maintaining a cash-pay model requires connections and expertise that money can't buy quickly.

Those licences and juicy stream of cash-pay markets will form a shield just as US health insurers dent the direct-to-consumer model at home.

The insurance threat

Cigna, one of America’s biggest insurers, has ordered its Evernorth pharmacy-benefit manager (the middleman that negotiates drug prices and runs every pharmacy claim) to cap Wegovy and Zepbound at $200 a month when prescribed for obesity.

Employer coverage is still new enough that Evernorth’s cap feels radical. A worker who once paid Hims $599 now pays $200, saves about $3600 a year - and that $200 also counts toward the worker’s annual out-of-pocket limit (the threshold after which the insurer pays everything).

Nine million people have joined Evernorth’s program in year one. At roughly 700,000 new members a month, Evernorth could top 15 million lives by 2026 and drain the D2C market - especially if other insurers follow suit.

The maths worries me and it worries wall street.

Bank of America stamped Hims with an Underperform rating—code for “we expect this to lag the S&P 500”—and a $28 target, roughly half the recent $60 share price, arguing that insurance companies will gut the company’s rich margins.

Coverage Goes Mainstream

Critics will argue that Evernorth is a one-off and bosses won’t foot the bill for obesity drugs. I disagree:

Employer adoption is rising. Last year, getting your employer to cover Wegovy was like pulling teeth. This year, 64% of America's largest employers now cover weight-loss drugs, up from 56% just twelve months ago. Even mid-size companies are joining the rush, with nearly half now offering coverage

Most hold-outs may switch. Integrated Benefits Institute finds only 12 % of plans still exclude weight-loss GLP-1s; 43 % of that group say they will add cover within 24 months. On that trajectory, over half the U.S workforce could have insurance coverage by 2026-2027

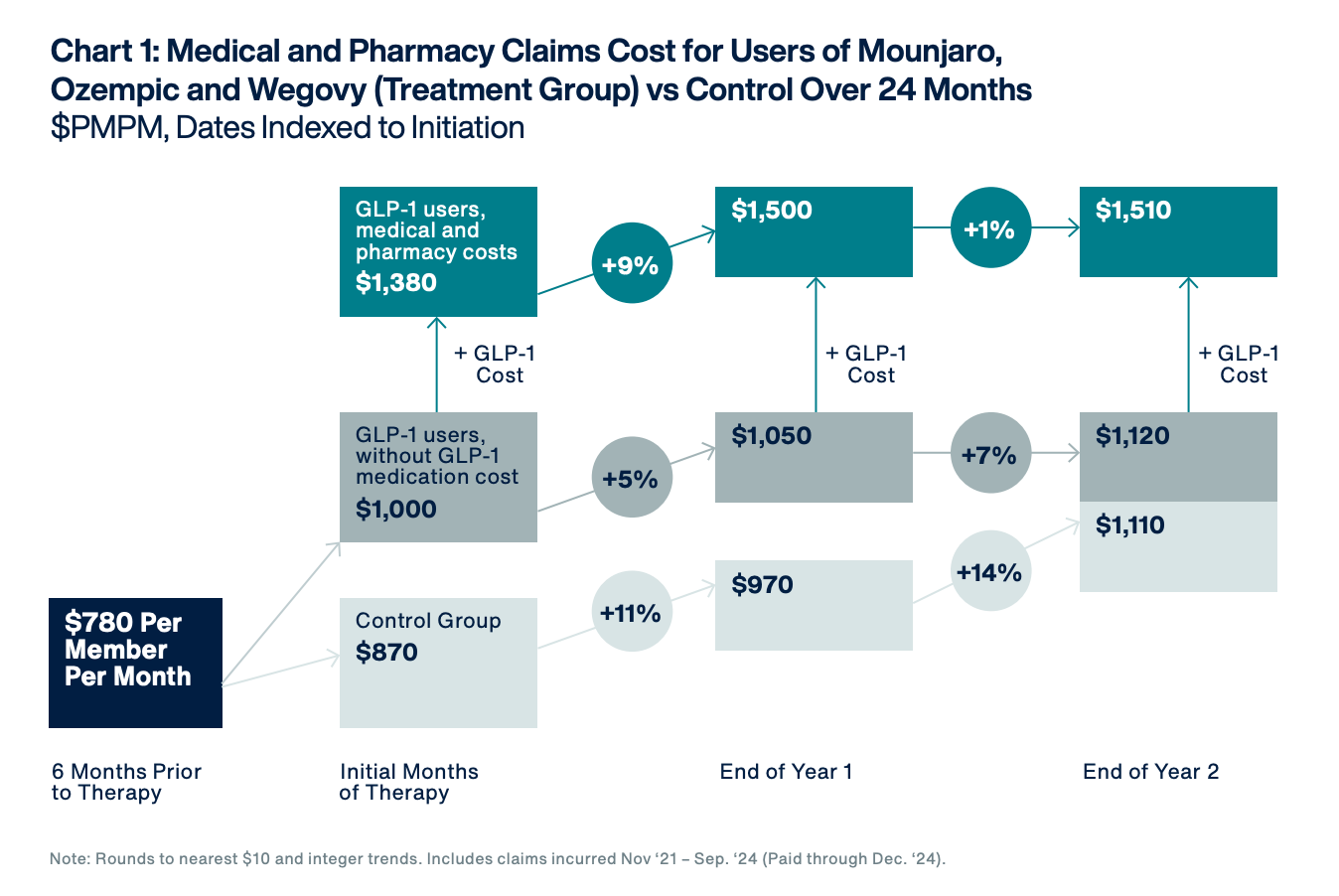

Return on investment is…getting there. Aon’s data tell two stories. First, GLP-1 users see their regular medical bills like hospital visits and doctor fees grow much more slowly than a similar group that never took the drug. Good news. But when you add in the price of the medication itself, total spending still ends up higher: about $1510 per person each month for GLP-1 users versus $1110 for the control group, a gap of roughly 35 percent after two years. In short, the drug quickly lowers other health costs, yet its own price more than wipes out the near-term savings which means employers won’t get true pay-back until the drug price drops or longer-term health gains kick in. I think that gap should narrow, though, as rival GLP-1s hit the market next year and will inevitably push prices down, giving employers a clearer path to real financial pay-back.

What the next move looks like

After raising $1 billion in convertible notes and sitting on another $300 million in cash, Hims has the firepower for at least one more platform acquisition. My prediction is that they’ll move into the Asian or Gulf markets within 12 months.

Asia's middle class is exploding—2 billion people and growing—with high out-of-pocket healthcare spending and minimal insurance coverage for obesity drugs. The Gulf states combine massive wealth, 20%+ obesity rates, and healthcare systems that favour cash-pay models.

Both regions are GLP-1 goldmines waiting to be tapped.

Striking now, while acquisition multiples are still pre-boom makes a lot of sense to me. Ro is probably eyeing international expansion. Noom may have teams scouting European partnerships. Every month Hims delays means watching competitors potentially grabbing these markets while acquisition multiples climb.

In the U.S., Hims needs to swallow its pride and link its pharmacy to the big pharmacy-benefit managers. Rival Ro already cracked this a while ago. They handle the online doctor visit and coaching, then route insured patients' prescriptions to in-network pharmacies. Ro earns a service fee instead of drug margins but reaches millions more buyers.

Why the hell hasn't Hims done this? Of course, it’s pure margin protection. Right now they charge $599 cash. With insurance, they'd get the same $30 fee CVS gets for filling prescriptions. But the alternative—watching their customer base evaporate as employers add coverage—is worse.

I think the smartest play is offering employers a wrap-around bundle: coaching, progress tracking and dose optimization. Prove the drugs cut overall healthcare costs and lock in steady subscription fees. It's the same playbook Embla already sells, and I like what they’re doing.

Conclusion

The Zava deal matters because it's a hedge against the American squeeze.

While U.S. insurers may bite the D2C model, Hims needs new cash-pay markets to fill the gap. One European acquisition won't offset losing half their American customers to employer coverage. They need multiple markets, Europe today, Asia tomorrow, the Gulf states after that.

This is why I think this move is more defensive than aggressive.

From where I’m standing, Hims just jumped from a helicopter. We are about to learn whether its chute is Swiss or made of gold-leaf.