India is not the opportunity you think it is

Why DTC telehealth won't work in India's GLP-1 market

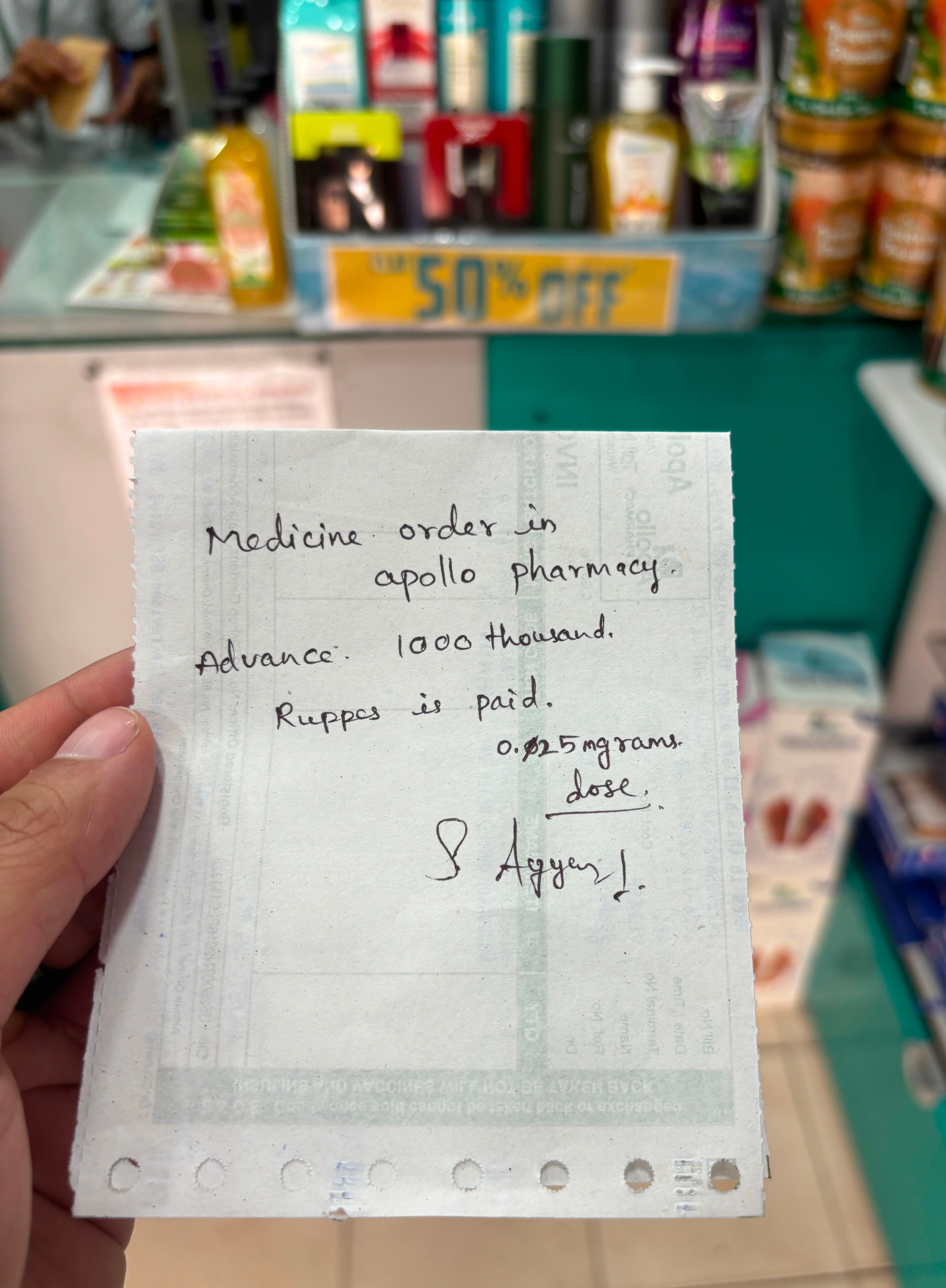

For the past two years, I’ve been visiting South India regularly, and I’d heard from many people that you can buy Ozempic over the counter without a prescription. So, on my last visit, I wanted to find out for myself. A few months ago, I walked into one of the most popular brick-and-mortar pharmacy chains and asked for 0.25mg of Ozempic. I put down a ₹1,000 (~$11) deposit, and sure enough, the pharmacist told me to come back to collect the pen. No prescription required and the whole thing took me about five minutes.

India runs on a principle best captured by a Hindi phrase that drives me nuts: “sab chalta hai,” which means “everything goes.” And, as I found, that also applies to “prescription-only” medication. In India, you can now buy semaglutide for less than a large oat milk latte at Starbucks. So, what exactly is the opportunity for direct-to-consumer telehealth companies looking to expand into this market?

DTC telehealth founders have spent the last two years pinning thumbtacks on a world map, hunting for the next market to enter, and now that semaglutide is off patent in India, it certainly seems like a gold-rush moment. But is the Indian market really where you want to place your bets?

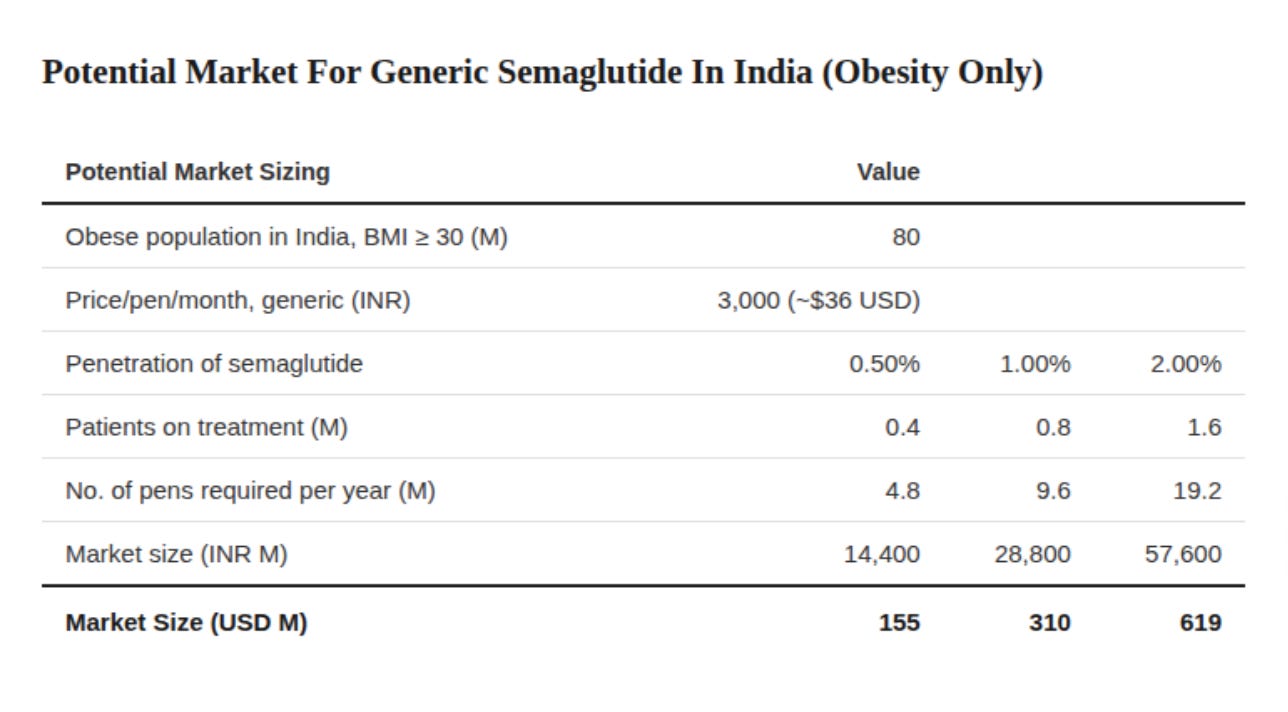

On paper, I understand the appeal: 14% of the world’s obese population lives in India, and those people are mostly in the middle and upper-middle classes. There is also a growing middle class and many digitally savvy consumers who are used to paying out of pocket for healthcare. My estimates show that the obesity-only GLP-1 market could exceed $600M USD if we assume a 2% penetration rate, though it would take a few years for the market to mature.

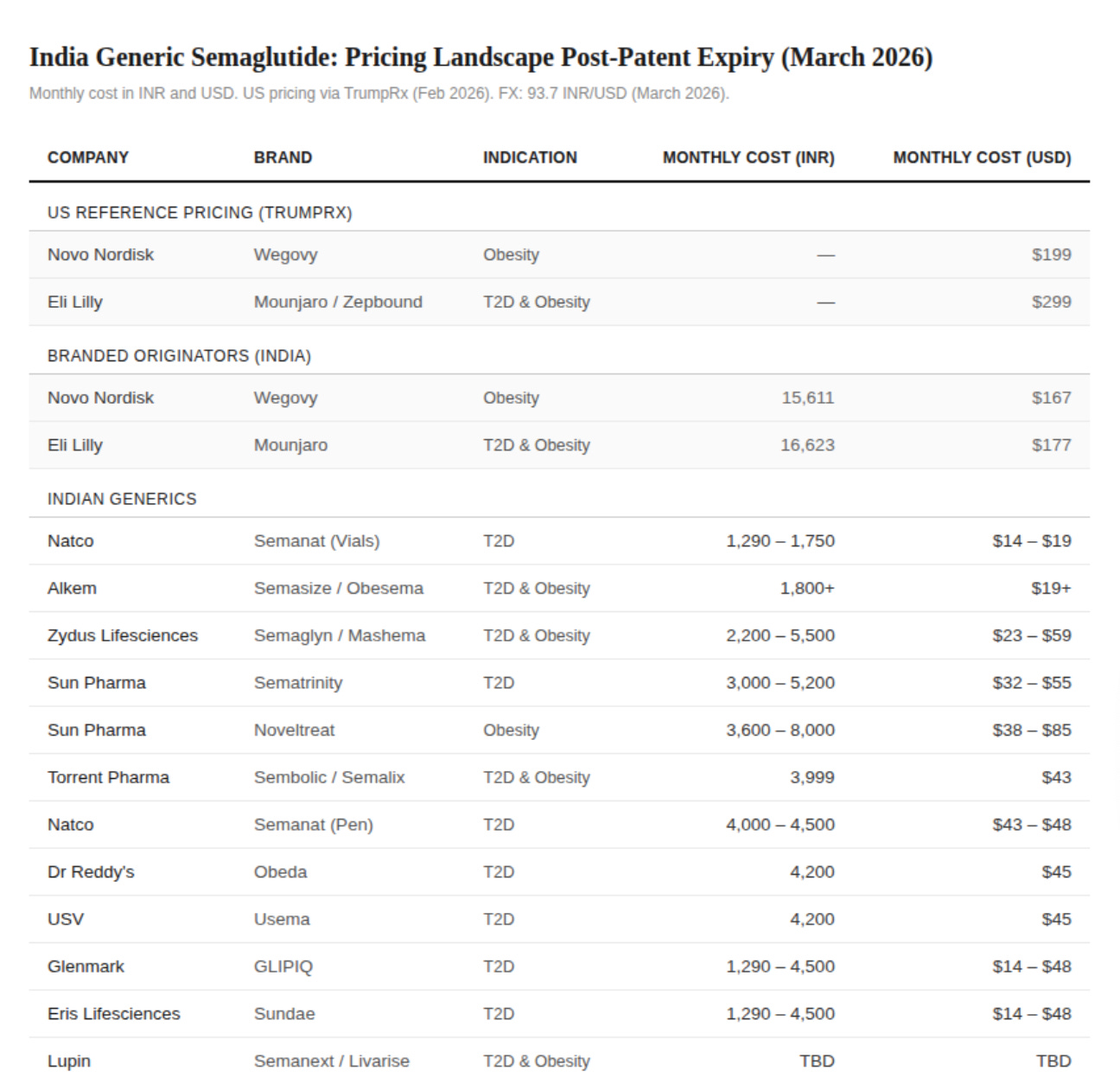

Several hundred million makes it sound like a market worth chasing, and a well-capitalised Western player could swoop in with aggressive marketing and a premium brand offering a nice and shiny subscription model to snatch up market share. But not everything that looks good on paper is worth the investment. Over 40 manufacturers are expected to launch generic semaglutide in the coming months, and several already have, at prices as low as $14 for a month’s dosage, which is enough of a price disparity to make people’s eyes water in the US (and mine, to be fair).

What we have on our hands is a commodity market with competition so fierce and margins so razor thin that manufacturers of semaglutide will become the first losers while those in the distribution-layer—like wholesalers, pharmacies, and e-pharmacies—will become the winners, because they own the relationship with the customer and decide which manufacturers get the volume. So, if distribution wins in a commodity market, then surely this is the moment for DTC telehealth to shine. Right?

Something new I'm trying with the Digest: spotlighting research that genuinely caught my attention

The team at Simple Online Pharmacy recently published Breaking the Silence, a white paper on the stigma around GLP-1 treatment in the UK, and it’s probably the most comprehensive snapshot of GLP-1 perception in the country right now.

After spending the better part of three years studying consumer behaviour around these drugs, it still baffles me how many people don’t recognise obesity as a chronic disease. Their report found that nearly half of UK adults don’t consider it a medical condition. And perhaps unsurprisingly, nearly two-thirds of patients won’t tell friends or family they’re on treatment!

That’s judgement rolled into treating weight as a moral failing rolled into a complete lack of scientific understanding. The knock-on effect is that people won’t talk openly about their treatment, and that has real consequences for people sticking around long enough to achieve good long-term health outcomes.

Very much worth reading the whole thing.

The Margin Problem

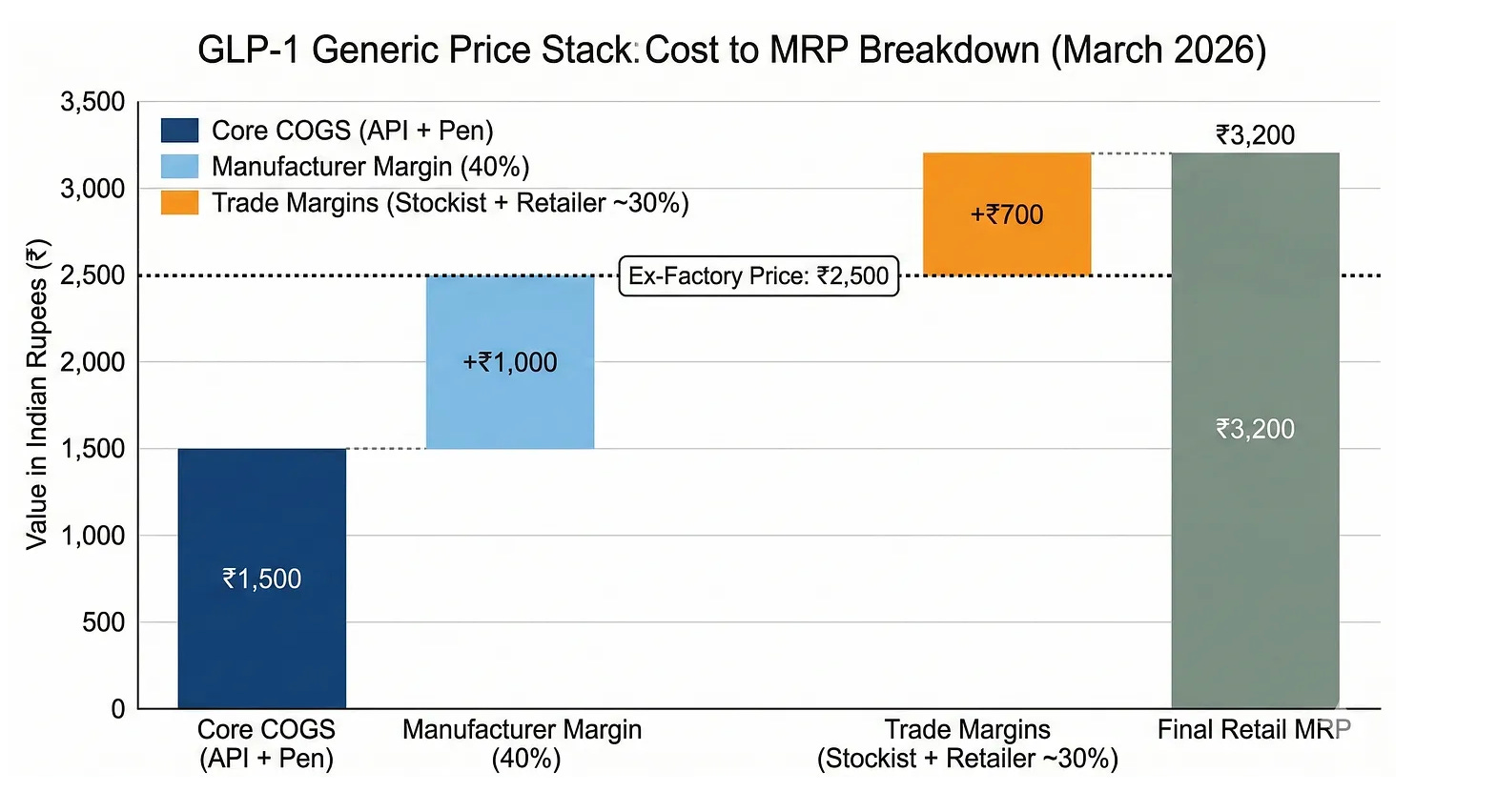

One glaring issue I want to highlight straight away is that some DTC players think they can waltz into India and make money simply by shipping the drug to consumers. They’re in for a rude awakening when they realize that it’s the manufacturer who sets the retail price, not the distributor.

Dr. Reddy’s, Sun Pharma, and Biocon print the “Maximum Retail Price” (MRP) on the medication box, which is the legal limit that no retailer, pharmacy, or platform can exceed. This is a key nuance of Indian economic law where the manufacturer controls the price rather than the market. This holds true for pharmaceutical drugs as it does for any packaged good, ranging from soft drinks and foodstuffs to shampoo.

In the case of generic semaglutide, which isn’t on India’s National List of Essential Medicines, there’s no government price cap, so the manufacturer works backward from the MRP and takes their margin at the ex-factory level first. The little margin that remains is what trickles down to the wholesaler and retailer.

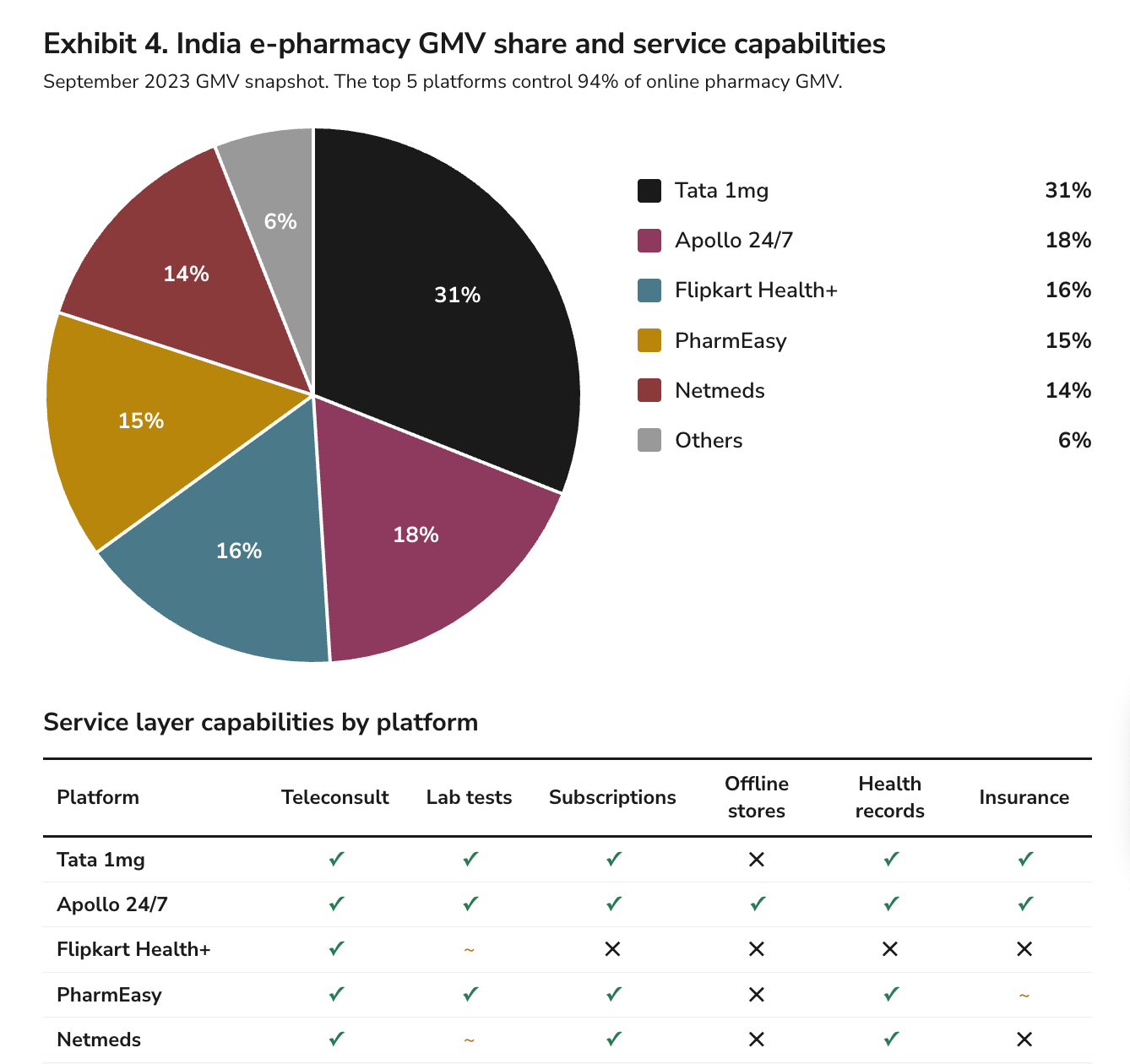

Since competition is so fierce among manufacturers, it’s likely that retail margins will be considerably better for incumbent e-pharmacy players in India, like Apollo Pharmacy, Tata 1mg, and Netmeds. These platforms already have millions of consumers buying medications through them every month, which gives them the leverage to negotiate better terms directly with manufacturers and bypass the margin-squeezed wholesaler entirely.

But those margins certainly won’t be flowing to the newcomers like Hims & Hers, HeliosX or Voy, if they’re trying to build distribution from scratch.

So, if you’re building a purely transactional service, you might be making a 20% margin, but the kill shot is that those margins don’t come close to making up the customer acquisition cost (CAC).

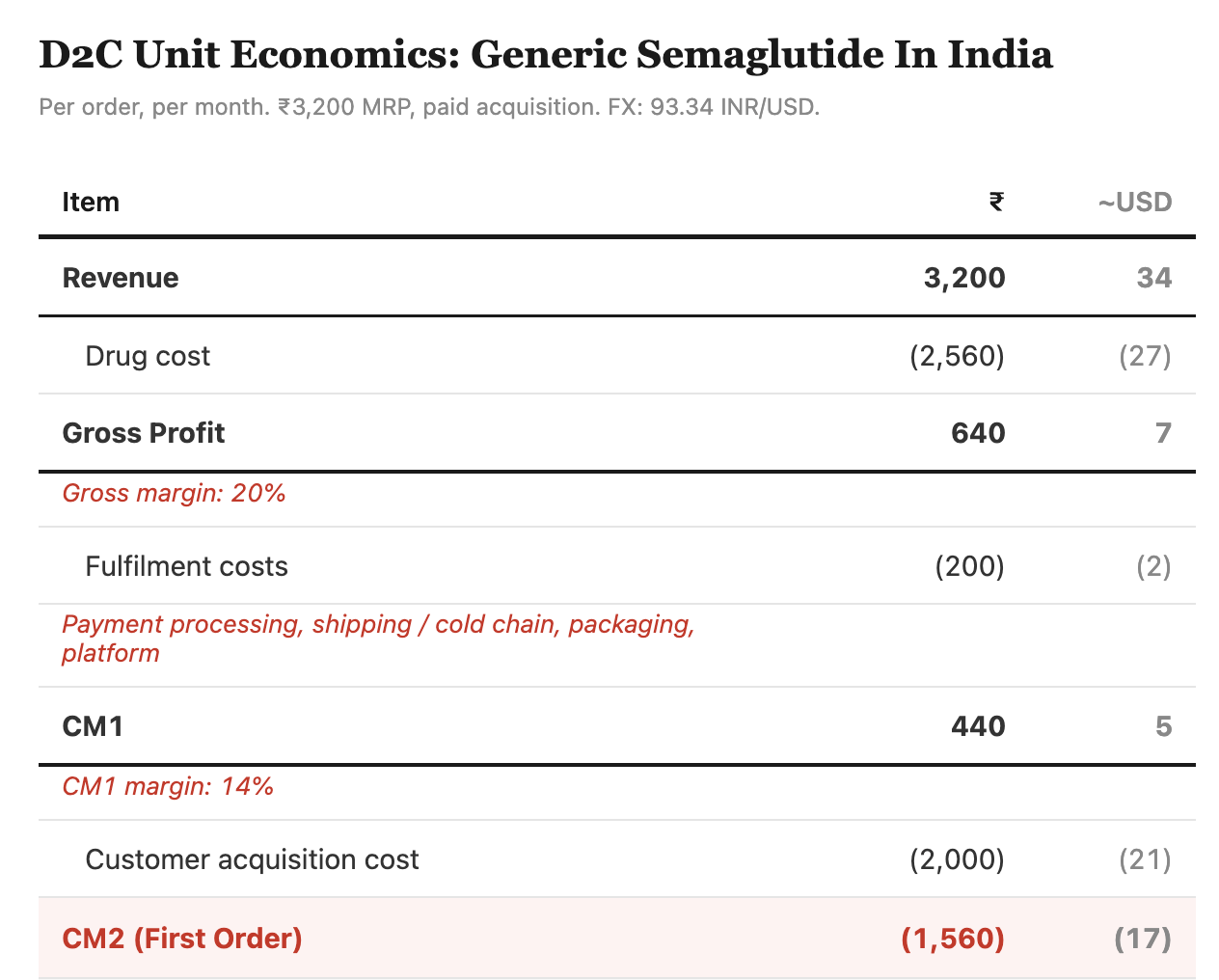

At an MRP of ₹3,200 (~$34) per month for a generic semaglutide pen, and assuming 80% of that goes to the drug cost, you’re left with ₹640 (~$4) in gross profit per order. After talking with some insiders, I estimate that for a single-category GLP-1 entrant, CAC is around ₹2,000 (~$21) per customer, which is probably on the lower side of the range.

That means it would take around 5 months to break even, and that scenario is optimistic, because it assumes that the customer actually sticks around. If CAC doubles to ₹4000, which is likely, given the competition between the e-pharmacy players, then it’ll take 9 months to recover CAC, which would require a herculean feat of customer retention.

Ultimately, the Indian market punishes low-margin chronic medication, unless you eliminate CAC (which you can’t do), raise prices (that you can’t set), or reduce supply (which you don’t own).

The Retention Problem

If those margins still sound doable, then we have to ask the obvious question about retention: Can you actually keep a customer on your platform for 5+ months when they could walk into any pharmacy and buy the same molecule for ₹1,000?

Indian consumers are historically price-sensitive and, unlike American consumers, have no brand-loyalty and no switching cost, which means retention is going to be the single biggest challenge for transactional players in India who have no way to differentiate themselves.

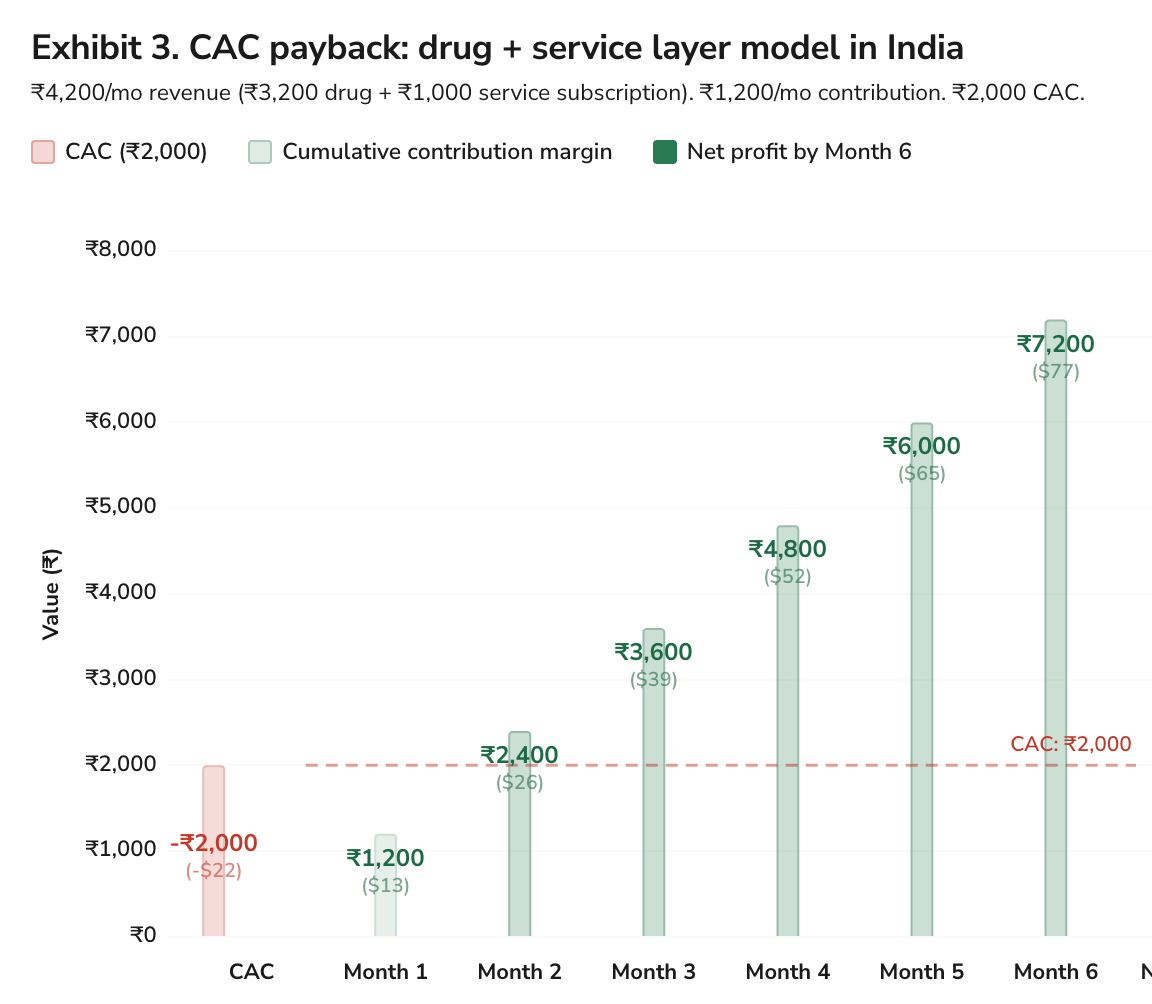

That’s why the service-layer is so important. While the drug price is fixed, you can add additional services like coaching or consultations through an app to increase margins. Health platforms offering wrap-around care can charge a premium and recover their CAC in a shorter time frame.

While this model is attractive and those service-based players should, theoretically, have a higher chance of retaining customers, the wrap-around care model is already well established in India and already packaged into most consumers’ expectations.

Apollo operationalizes shipping + consultations + diagnostics as one integrated experience, while Tata 1mg has normalized “doctor consultations on chat,” “lab tests at home,” and subscription-based care-plans.

Similarly, Netmeds runs a membership layer (cashback + lab discounts) and positions consultations, labs, and records as some of their core features. Lots of these incumbents also deliver the medication on the same day, and often within 30 minutes to 2 hours in most of the metropolitan areas. So, as above with the distribution problem, it’s gonna be tough for any newcomers to differentiate themselves from the platforms that have been in the market for years.

Conclusion

Generic semaglutide arriving in India is, on balance, a genuinely good thing. Eighty million people with obesity will have access to a drug that will completely change their health. That level of accessibility not only unlocks better health but also more economic productivity through reduced sick days and fewer obesity-related complications. It’s hard not to be optimistic about the health of India’s population over the next decade.

But for DTC telehealth founders looking for the next hundred-million-dollar revenue stream, I struggle to see that opportunity. As another country with patent-expiry looming, India is now a commodity market for GLP-1s but one with retail-price caps, entrenched distribution, and no prescription enforcement.

If you’re still seriously considering India after everything I’ve laid out, then at the very least, you need boots on the ground and a local team who understands the consumer. Forget selling the drug, because the margin isn’t there. Instead, partner with a manufacturer who needs a digital channel, and build an army of doctors who are prescribing the drugs in clinics so that you aren’t relying on marketing as your only method of customer acquisition.

Nonetheless, sometimes the biggest opportunity is recognizing when to pass.

**The views, opinions, and recommendations expressed in this podcast and essay are solely my own and do not represent the views, policies, or positions of any other organization with which I am affiliated. This content is provided for informational purposes only and should not be considered medical, legal or investment advice.**

Very interesting analysis. It made me think that if Lilly wants to be the leader in India they have a clear path to do so with Orfo, which based on your math and insight on the indian market dynamics, would seem to be a better fit, especially wrt margin. Whether they push to market in India themselves or in partnership with an Indian co (as an authorized generic maybe) or some hybrid will be interesting.