The $100 Billion Overreaction

how do oral GLP-1s expand the market?

I keep wondering how much orals will really change the obesity landscape. Wall Street is fixated on weight-loss percentages, while analysts throw around wildly different penetration numbers. Some say orals will make up just 25 percent of the obesity market, others think it could be closer to 75 percent. But I really think that framing misses the point because it treats orals as if they are competing head-to-head with injectables.

They’re not.

So in this issue:

Why orforglipron is okay, actually

Wegovy is experiencing significant tailwinds

Sponsorships

These are just the first skirmishes in a much, much bigger story. Over the next few issues I’ll be digging deeper into the divide between peptides and small molecules, and what that means for the future of obesity drugs. If you like to nerd out on this stuff, you’re in the right place.

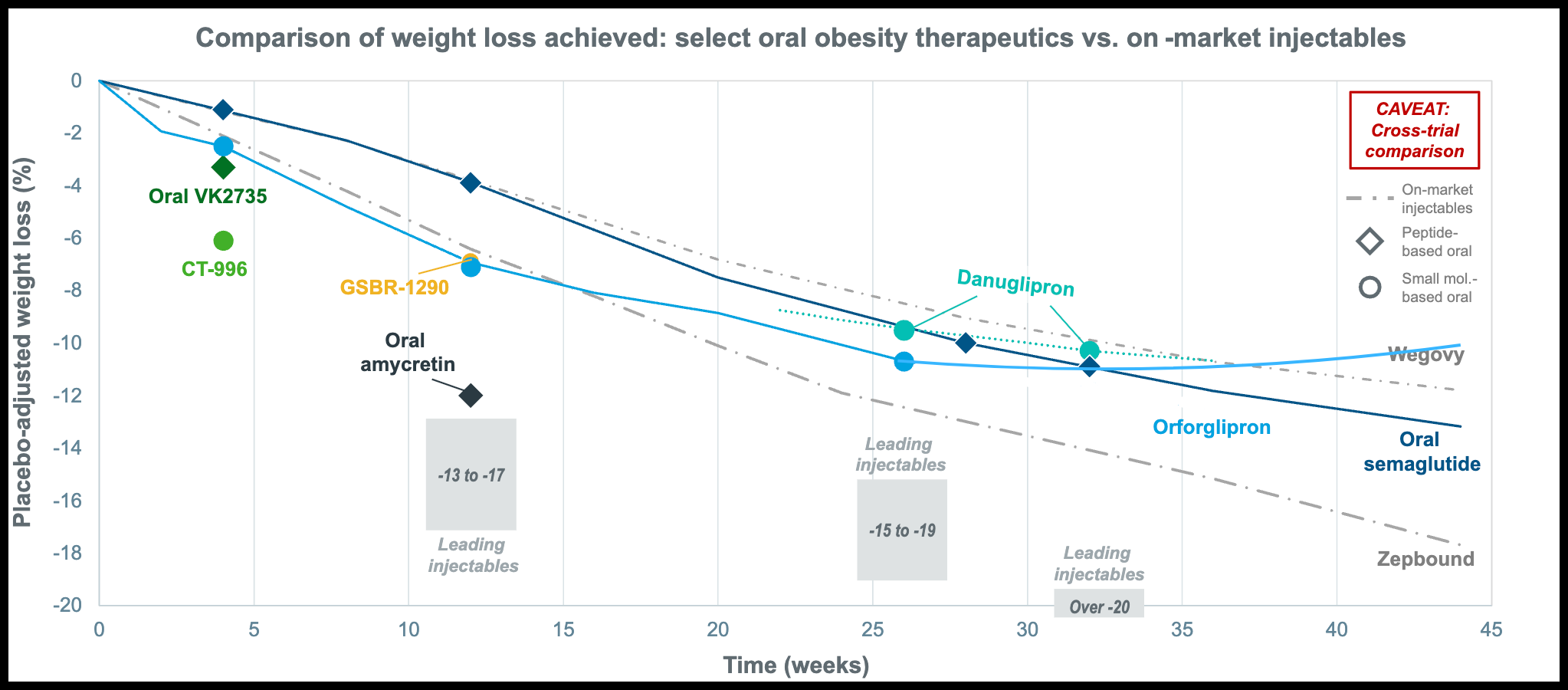

Wall Street Got Orforglipron Wrong. The market's knee-jerk reaction to orforglipron's Phase 3 data, which wiped nearly $100 billion off Eli Lilly's market cap, says more about Wall Street's tunnel vision than the drug's actual potential.

Yes, orforglipron's 9% placebo-adjusted weight loss came in below injectable Wegovy's 12.6%.

But treating a three-point gap like a disaster completely misses the point of oral GLP-1s.

Their job is not to out wegovy-wegovy, rather it’s to widen the funnel. Someone looking to lose 10-15 pounds on the lower end of the disease spectrum, or those who find weekly shots intimidating, are far more likely to start with a daily pill.

Once they’re in the “GLP-1 ecosystem”, I expect many will naturally progress to the more potent injectables like Zepbound when they hit weight loss plateaus. In that sense, this patient-led progression makes orforglipron a lead generator feeding Lilly’s ‘premium’ franchise.

The next challenge is keeping people in the ecosystem and this is where orforglipron will serve as an important retention tool. Patients who hit their goal weight on injectables struggle with the idea of weekly shots for life, and a pill is a much softer, more ‘digestible’ option for holding on to those gains and reducing relapse.

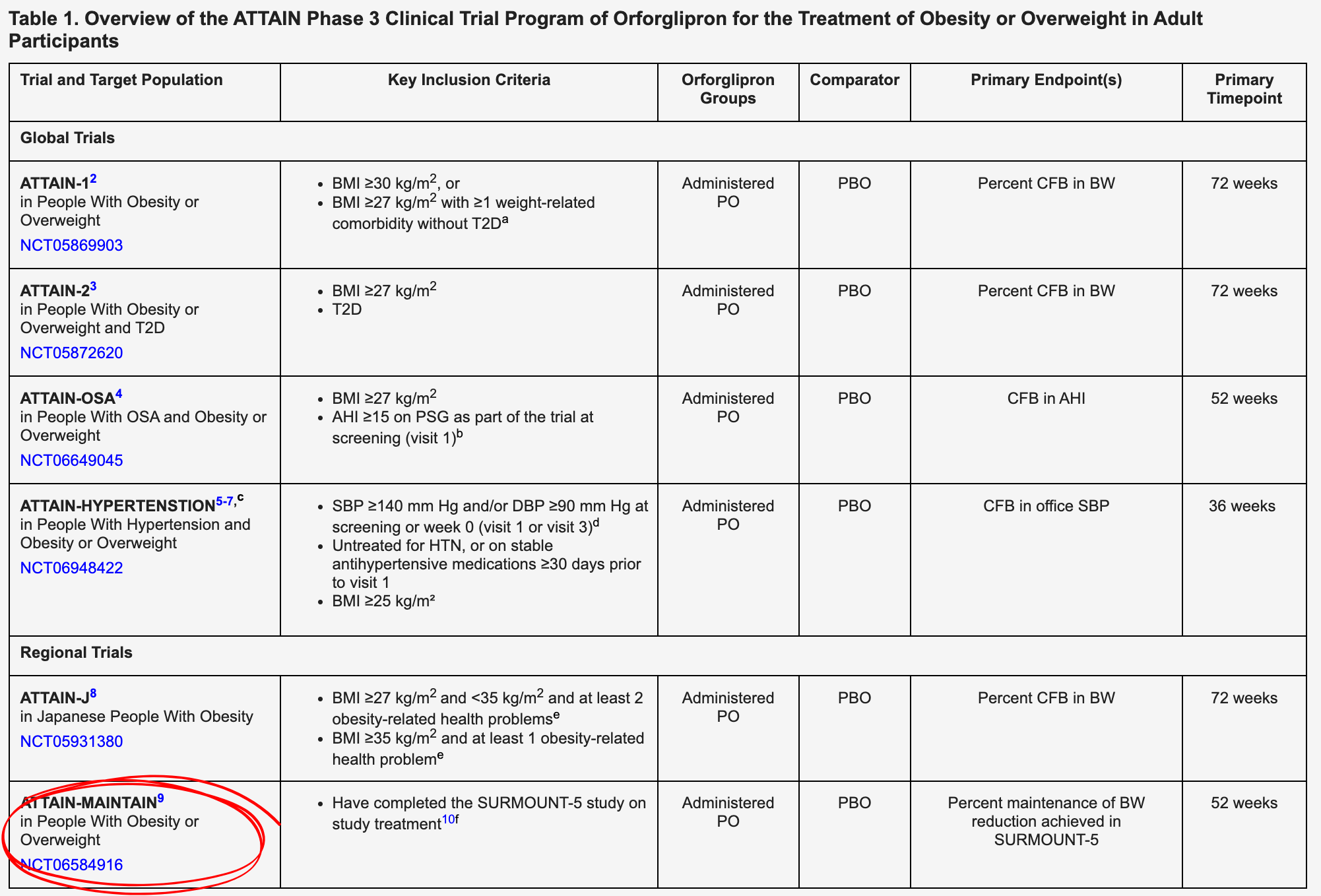

Lilly has shown particular foresight here, being the only pharma company asking the obvious but un-answered question: what does maintenance really mean?

The ATTAIN-MAINTAIN trial reframes obesity care as a two-stage journey — attain weight loss with high-potency injectables, and then maintain it with a lower-burden oral. If the data supports that model, Lilly will be selling the first treatment ladder for long term obesity care.

However, pricing is the elephant in the room because none of this matters if patients can’t actually afford the drug. In the insurance channel, Lilly will almost certainly follow the same playbook Novo Nordisk used with Rybelsus.

When Novo launched its first oral GLP-1, investors expected a discount, assuming a pill would be positioned below injectables. Instead, Novo priced Rybelsus at near-parity with Ozempic — roughly $770 a month — a decision cleverly designed to avoid the perception of being the “cheap alternative” and to protect the premium positioning of its injectable franchise. This preserved negotiating leverage with insurers, while the real price patients paid emerged through the familiar dance of rebates and backroom deals.

Lilly has every incentive to do the same with orforglipron.

If Lilly were to list the pill too low, payers could seize on that price point and force every patient through step therapy, requiring them to fail the oral before approving injectables which would of course cannibalize injectable sales.

To avoid that trap, Lilly will keep orforglipron’s list price at parity with injectables — roughly $900 to $1,300 a month and let the true net price shake out quietly in negotiations.

This probably means high list price for optics.

But cash-pay is where things get very interesting. On the last earnings call, CEO David Ricks hinted at “consumer-level pricing” for orforglipron which is code for going straight to millions of uninsured or underinsured patients.

Zepbound has shown how powerful this can be, with cash-pay accounting for one in five total prescriptions and more than a third of new ones in Q2. The difference is that orforglipron, as a small molecule with rock-bottom manufacturing costs, gives Lilly far more flexibility.

If Zepbound can thrive at $349 a month, orforglipron could plausibly come in at $150–300 which is low enough to capture uninsured demand at scale.

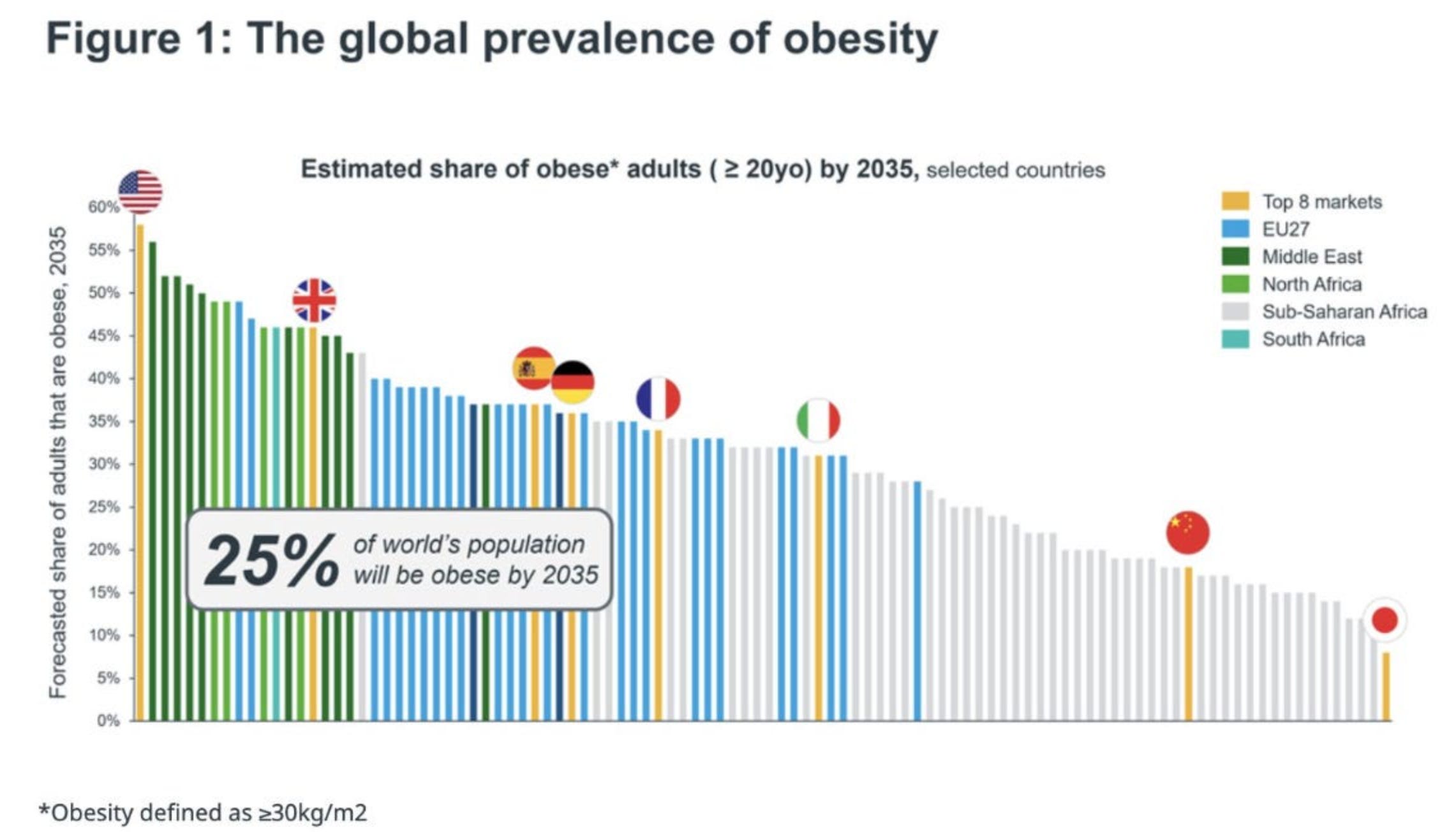

These manufacturing advantages matter even more from a public health stand point. By 2035, nearly 80% of adults with overweight or obesity will live in low- and middle-income countries. These are the markets where weekly peptide injections can’t scale because they require cold-chain storage and reliable infrastructure for transportation. Most emerging economies won’t have that, especially in hotter regions where maintaining refrigeration is extremely difficult.

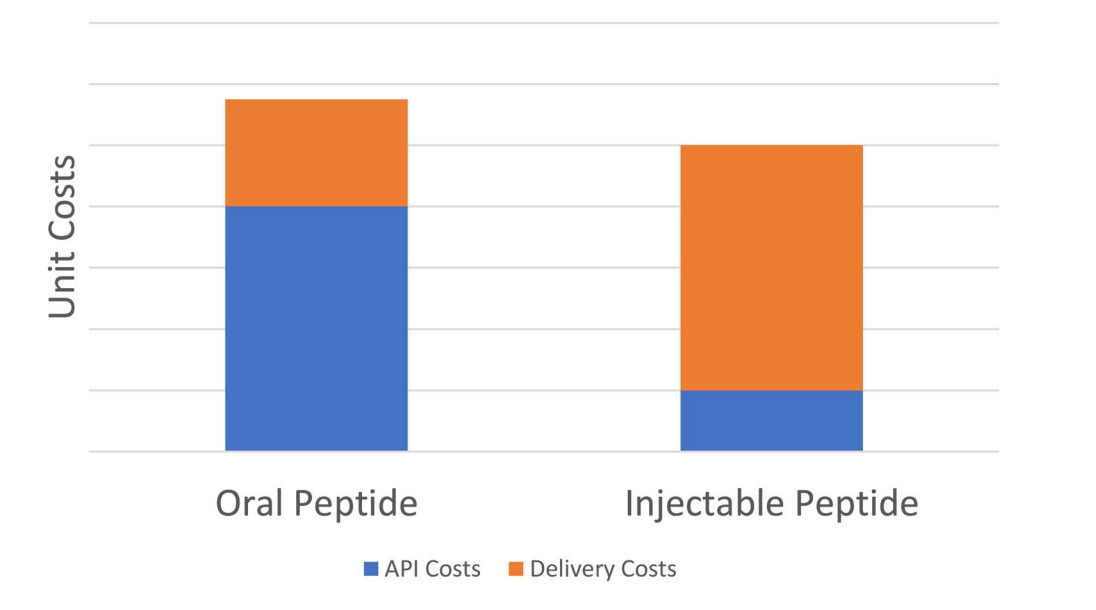

This is why orforglipron is so compelling. It can be manufactured in standard pill plants, stored at room temperature, and shipped anywhere. Oral semaglutide, by contrast, is far more complex and expensive to make. It requires unusually high amounts of API per pill — orders of magnitude higher than injectables — which drives up cost of goods and limits scalability. On top of that, patients must fast for at least 30 minutes after taking it, a daily friction point that makes long-term adherence harder. Orforglipron avoids both problems which in my view makes it the only oral GLP-1 candidate with a credible path to solving the global obesity epidemic.

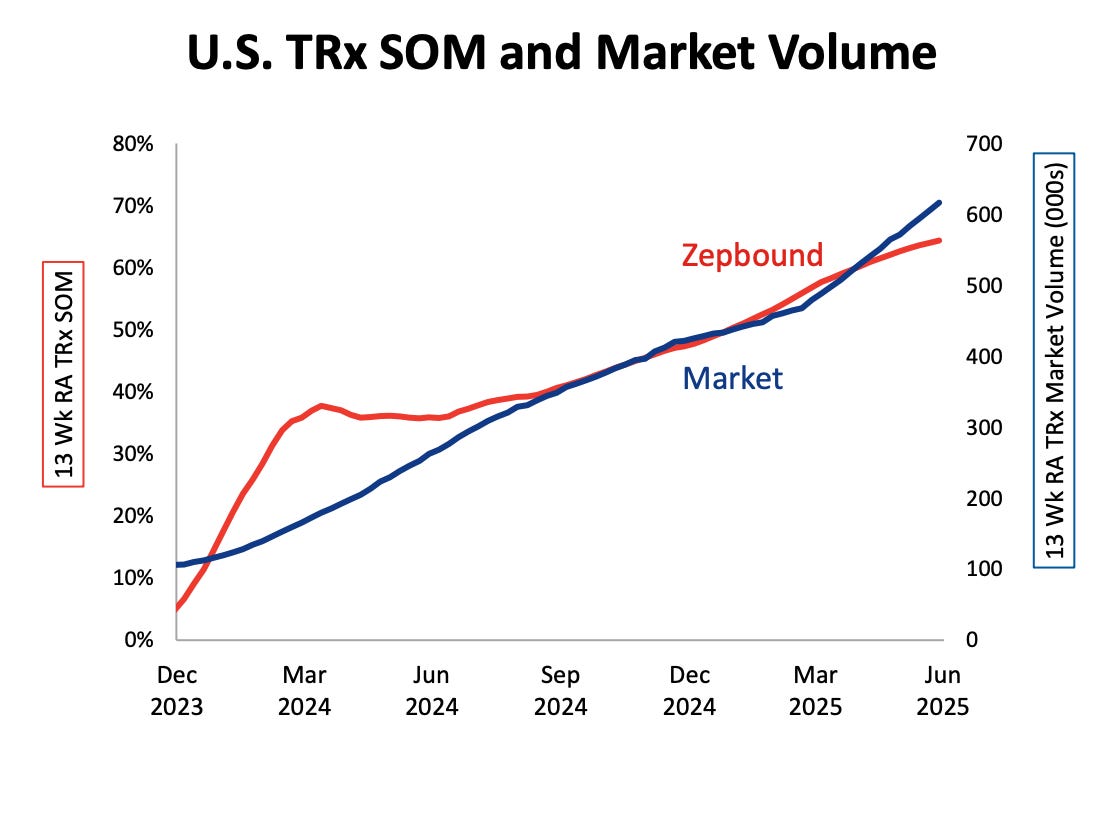

Wegovy sells. UK online pharmacy CheqUp reported a 27-fold surge in Wegovy sales — a 2,660% jump compared with the daily average in July— with the lowest dose up more than 2,200% as new patients flood in.

The positive development is the result of a uniquely favourable set of tailwinds. First, Eli Lilly’s UK price hikes created a clear cost advantage for Wegovy. Second, the timing coincided with the post-summer health reset when people return from the holidays and decide to commit to constructive action after two months of sun and fun.

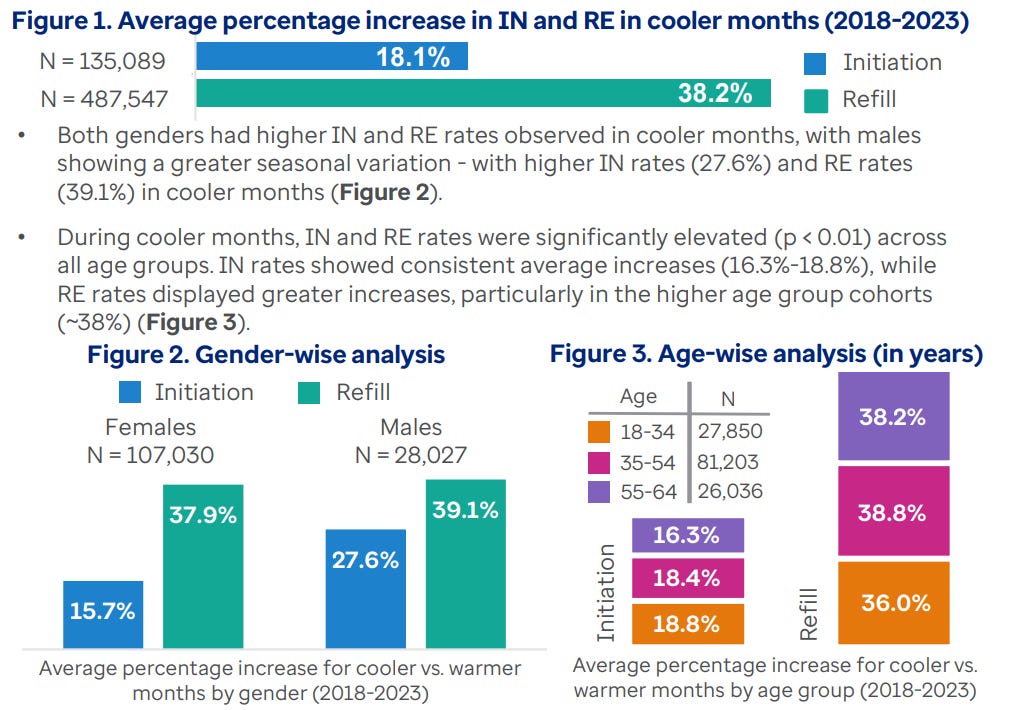

This is a very interesting seasonal pattern that shows up clearly in GLP-1 initiation and refill data.

The increase in sales for Wegovy is predictable enough, as I wrote about in detail last week. But the real question still is whether the company can sustain momentum. Price shocks and seasonal resets can fill the funnel in the short term, but the longer game is still supply and access.

Novo has the wind at its back, but a) for how long? and b) can they keep up with the demand now or will there be another shortage? Time will tell.

Sponsorships. For the first time, I’m opening up a sponsor slot for the autumn. In the past three months, this newsletter has grown beyond all expectations, and now lands in the inboxes of 1,100+ founders, investors, and senior health tech executives. These are the people writing the cheques, building the companies, and shaping the future of healthcare. If you want your brand in front of them, email me at ash.sharma@live.co.uk.

**The views, opinions, and recommendations expressed in this essay are solely my own and do not represent the views, policies, or positions of my employer or any other organization with which I am affiliated. This content is provided for informational purposes only and should not be considered medical, legal or investment advice.**