What happens when GLP-1s go off-patent?

Five charts that’ve caught my eye

In this issue, I’m experimenting with a new format: five graphs that have caught my eye over the past fortnight. I’ve been thinking about how this data feeds into the bigger narratives playing out in GLP-1 and cardio-metabolic health spaces, which are wide and varied as you’ll see. These are not the top-five of anything but, rather, five charts that I personally can’t stop thinking about.

Now, let’s get to it.

Is the GLP-1 market overpriced?

I’m only now coming to terms with the fact that the obesity market may be overpriced. In many ways I’m shooting myself in the foot here, given that I’m trying to build a niche B2B media company in this space, but I strongly believe that is all secondary to truth-seeking.

In my view, the obesity market is running too hot because analysts are cranking up their sales-volume projections for new drugs in the pipeline while underestimating how much generic semaglutide will erode the market share of those name-brand drugs’.

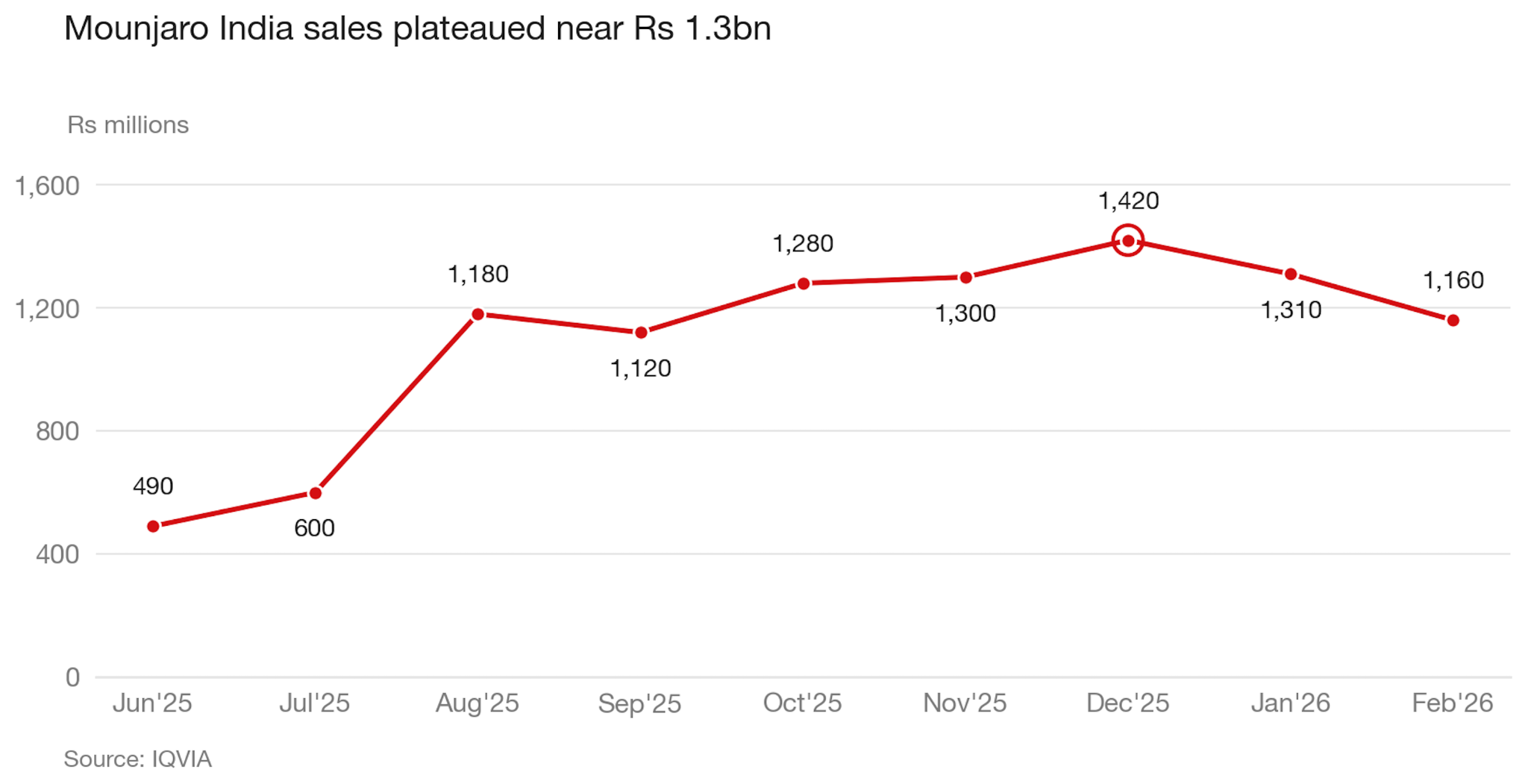

If you look at India, which I’ve been glued to lately, manufacturers have flooded the market with cheap, generic semaglutide and in the space of just one month, it’s eroded Mounjaro’s market share by an estimated 7%.

Given that Mounjaro became the best-selling drug in Indian history, and has a better weight-loss profile than Sema (with similar side effects), I’m confident the same dynamic will play out in the UK and US when semaglutide goes off patent in 2032.

Once that happens, I believe it’ll severely dent the market share of Cagrisema (Novo), Retratrutide (Lilly), Survoutide (Boehringer Ingelheim), and MariTide (Amgen)—all of which are expected to enter the market between 2027 and 2029.

The problem is that GLP-1 medications are joined at the hip. It doesn’t matter if it’s Wegovy or Mounjaro, 20% efficacy or 25% efficacy—hell, even 30% efficacy. When one of these medications goes off patent, the branded medication shares will decline, because incremental improvements in efficacy or tolerability will not be enough to convince price-sensitive consumers or insurers or healthcare systems to fork over a premium when there’s a ‘good enough’ semaglutide for $60, versus a $6,000 retatrutide.

Unless one of the new pipeline drugs shows another differentiator like alzheimer protection, or becomes combined with something like a myostatin inhibitor that can protect muscle-mass loss, then I believe we’re going to see the semaglutide patent release cause a nosedive for every other branded GLP-1 on the market in 2032.

Will oral GLP-1s cannibalize injectable sales?

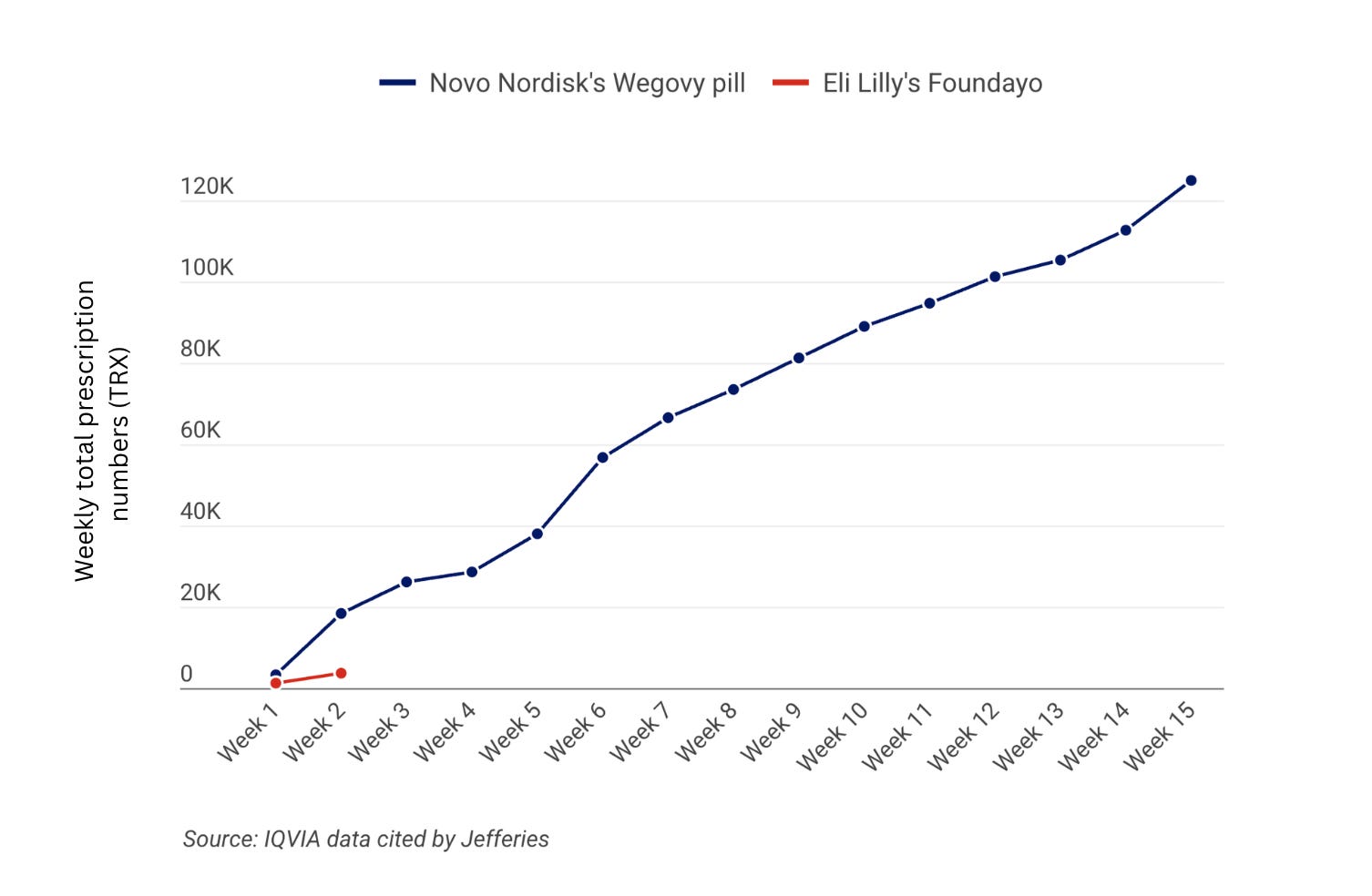

We’re approaching the end of the 4-month mark since oral Wegovy’s launch, and the success has surprised everyone, including me. Novo has developed a strong lead with UBS’s forecasts projecting 400k total prescriptions at the end of Q1, with the majority of sales coming through cash-pay channels capturing net-new GLP-1 users.

Foundayo is off to an okay-ish start with 3,707 prescriptions in its first two weeks of launch, compared to oral Wegovy’s 18,410 prescriptions.

However, I expect that oral Wegovy sales will begin to tinker down over the coming weeks, as competition heats up. Foundayo and Wegovy are similarly priced for the starting doses and are fighting for the same type of patient (needle-averse, price-sensitive).

But, with the rise of oral GLP-1s, the big question is how much the pills will cannibalize the injectable market, and in my view, it won’t be much at all.

There are a few reasons why I believe this.

First, pricing for oral Sema, Foundayo and injectable Wegovy cluster around similar price points of $149–$349, which gives us something close to a controlled experiment. If prices are roughly the same, the only thing left for a patient to optimise around is preference.

For some people a pill is obviously the easier option because they’ve taken tablets their whole life. For others, a weekly jab is the easier option because one decision a week beats 365 decisions a year, especially when the pill comes with a 30-minute fasting window or drug-drug interactions (like Foundayo) which increase friction.

Second, I have higher conviction that patients on a daily oral pill may switch to an injectable over time, primarily driven by perceptions of weaker efficacy.

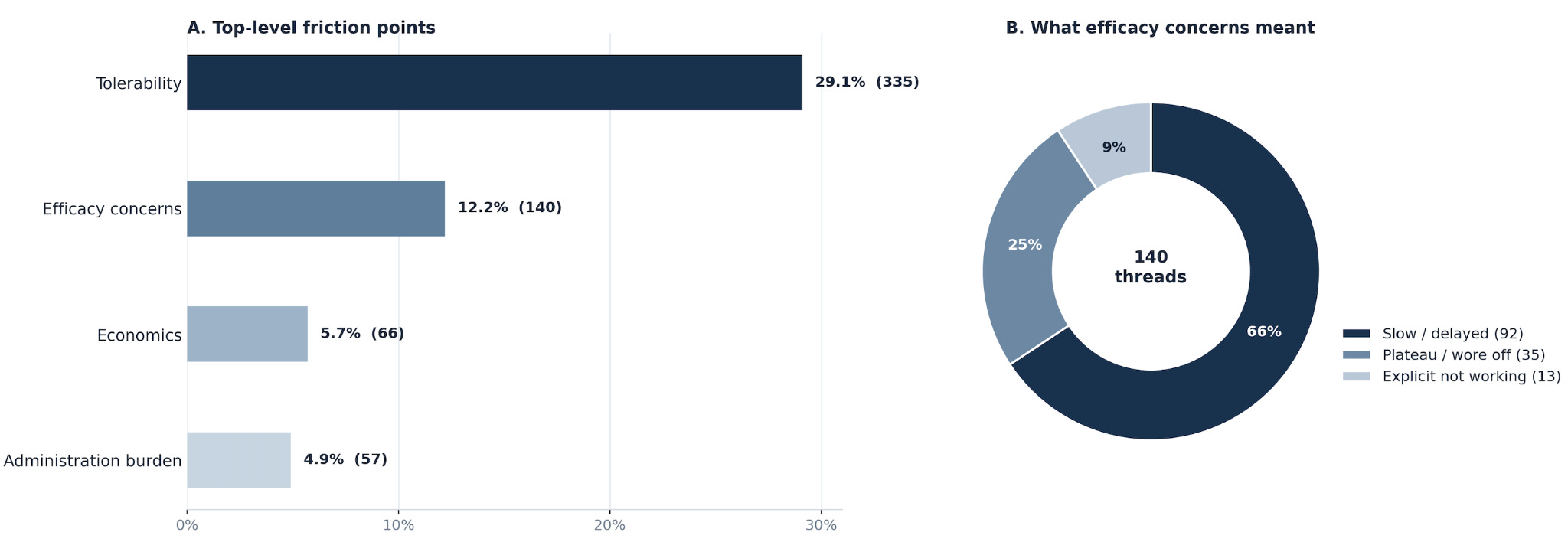

To pressure-test this, I ran a social listening scrape across r/WegovyPillWeightLoss, r/WegovyWeightLoss, and r/Wegovy on 23rd April 2026. From 2,897 threads (post + comments) I filtered down to 1,152 oral-only discussions and coded them across side effects, efficacy, cost and access, and other themes.

My analysis showed that roughly one in eight oral-only discussions were about efficacy concerns, and the vast majority reported slow responses to the drug or appetite/food noise coming back.

I believe this is the group most likely to switch to injectable therapy (Wegovy/Mounjaro), because injections will be seen as a stronger or even a more dependable option. And, I expect this cohort to get pretty big, because GLP-1 patients have mismatched expectations (fuelled by social media and AI slop), believing they should be dropping 20lbs a month on these drugs.

How to improve DTC retention

If you’re a GLP-1 patient, a lot has to go right in months one to three. You’ve got an onboarding form here, a pharmacy portal there, a coaching app on your phone, and a telehealth link buried in an email. Want to re-order? That’s one login. Check your next consult? Another. Talk to a prescriber? Good luck finding the link.

Most patients don’t bother, and they churn when friction is high and cognitive load is higher.

This is where Light-it comes in. They’re the healthcare product and engineering team behind some of the fastest-growing GLP-1 telehealth platforms, and they've been a sponsor of GLP-1 Digest since the beginning.

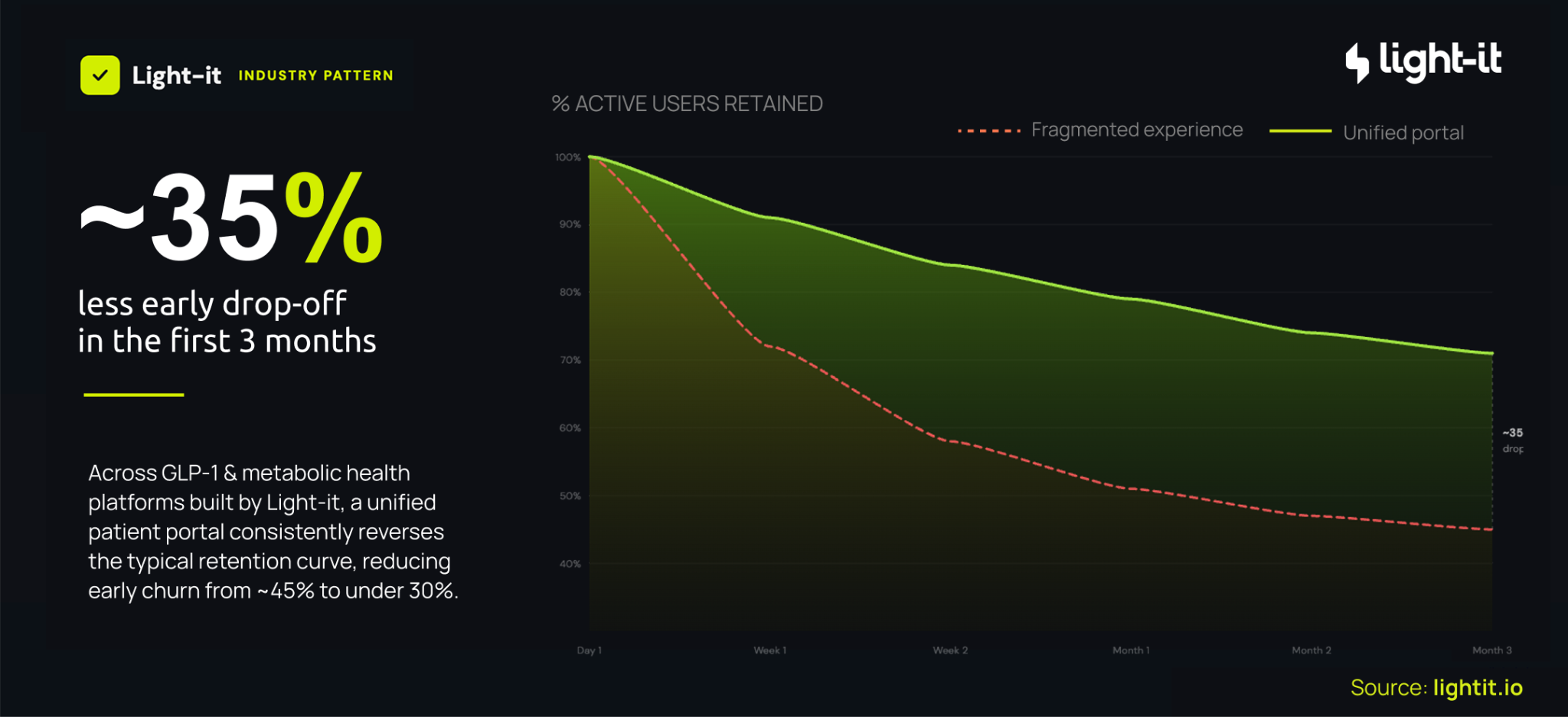

Across the platforms they’ve built, where onboarding, telehealth, prescriptions and coaching all sit inside a single patient portal, early drop-off runs at around 35% over the first three months.

On fragmented setups it’s more than 50%.

That’s a huge ROI improvement, because if you can lift retention by even a few points, that compounds across thousands, if not hundreds of thousands of patients, and bolsters your customer lifetime value.

If you’re a telehealth provider and your retention curve looks more like the red line than the green one, talk to Light-it. They’re the product and engineering team behind several of the GLP-1 platforms you’ve already heard of.

Canadian insurance can cover it

Canada is not a viable market for D2C GLP-1 expansion. Approximately 75-80% of Canadians have medical insurance through their employer, and I believe the vast majority of those health plans will begin to cover generic semaglutide for weight loss once the drugs are approved by Health Canada. Generic pricing will come down by at least 40–70% which is cheap enough that refusing coverage will become politically indefensible.

That leaves a tiny residual pool of uninsured and patchy-coverage patients paying out of pocket to D2C telehealth players like Felix. Given the Canadian obesity market is already small, the remaining serviceable market is a sliver of a sliver.

To be profitable then, a D2C platform would need patients to pay a premium for one of two things where they can make margin. Either a differentiated formulation, like compounded generic semaglutide with B12 or whatever else, or a high-touch service layer that’ll keep patients on the platform.

I’m not convinced that either method holds up. Compounded formulations stole large market share in the US because they undercut Novo’s branded pricing by 60–70%, which created the cash-pay arbitrage that turbocharged growth for Hims. That arbitrage doesn’t exist in Canada, because the generic is already going to be so cheap, so there’s nothing for a compounder to undercut.

For the premium service layer, I do think some patients will pay for white-glove care, coaching, and continuity, and there’s a legitimate business in serving them. It’s just not a venture-scale business.

In my view, the economics of the Canadian market is purely an information-gathering exercise in how a Western market responds to generic GLP-1s. But for D2C companies looking to expand, that’s all it is.

**The views, opinions, and recommendations expressed in this essay are solely my own and do not represent the views, policies, or positions of any other organization with which I am affiliated. This content is provided for informational purposes only and should not be considered medical, legal or investment advice.**

I think a big unknown for me is how strong private US insurance coverage is going to be before sema goes off patent. Demand is quite high and that can tick up premiums in exchange for coverage. A lot of insurers still won't cover GLP-1s or place huge barriers to access. Also still seems to be little short-term ROI for an insurer covering weight loss meds even with MACE benefits in hand. I think you're right that the data will need to show more benefits of taking GLP-1s, especially shorter-term benefits that fit within the 3-5 year ROI window of these private plans. Once its generic, that makes coverage way easier. But I wonder if in 2032+ we'll be in a place where if you want "average" weight loss you can go through insurance, but if you want "massive" weight loss you pay with cash for one of the more effective next-gen agents. Just food for thought.

The oral story is really interesting too. Obviously with a small molecule like FOUNDAYO, you have way more margin to play with and can reduce price to gain market share. But I wonder if the ultimate most-common use cases for orals ends up being as maintenance. Take your reta/tirz to get down to your ideal weight, then switch to an oral to maintain.