Being a MD and sifting through medical papers, you learn to spot the statistical sleight of hand and the ways scientists p-hack their way into favourable results that make a mediocre finding seem groundbreaking. I’m learning that earnings calls and shareholder letters work much the same way.

The thing is, though, no matter how convoluted an academic paper or earnings report is, numbers never lie. You just need someone who can figure out what the hell is going on under the hood.

That’s why I was so glad to sit down with Paul Cerro to break down Hims & Hers’ latest earnings report.

Paul is the Chief Investment Officer and Founder of Cedar Grove Capital Management, a registered investment advisor based in Michigan. Before that, he was an investment banker at Merrill Lynch and worked in strategy at Ro.

Last year, I came across Paul’s work on D2C telehealth companies, and the caliber of his analysis made me an instant fan. Case in point: 12 months ago, Paul predicted the HIMS stock price to within 40 cents of where it landed at the end of 2025, which is absolutely astonishing and earned him the favor of detractors who’d spent months trying to discredit his thesis.

For full disclosure, Paul has a short position on Hims & Hers, and he’s one of the most prominent bears on the stock.

What follows is a breakdown of our conversation. We pull apart the Q4 2025 earnings and trace the common threads quarter over quarter. This is not an ultra-bearish hit-piece, and I’ve tried to keep it fair. Paul even offers a steelman argument for how Hims could succeed, but the numbers make the situation harder to spin than management would like.

Here are my three biggest takeaways, though I urge you to listen to the full episode, because the detail is where it gets really interesting.

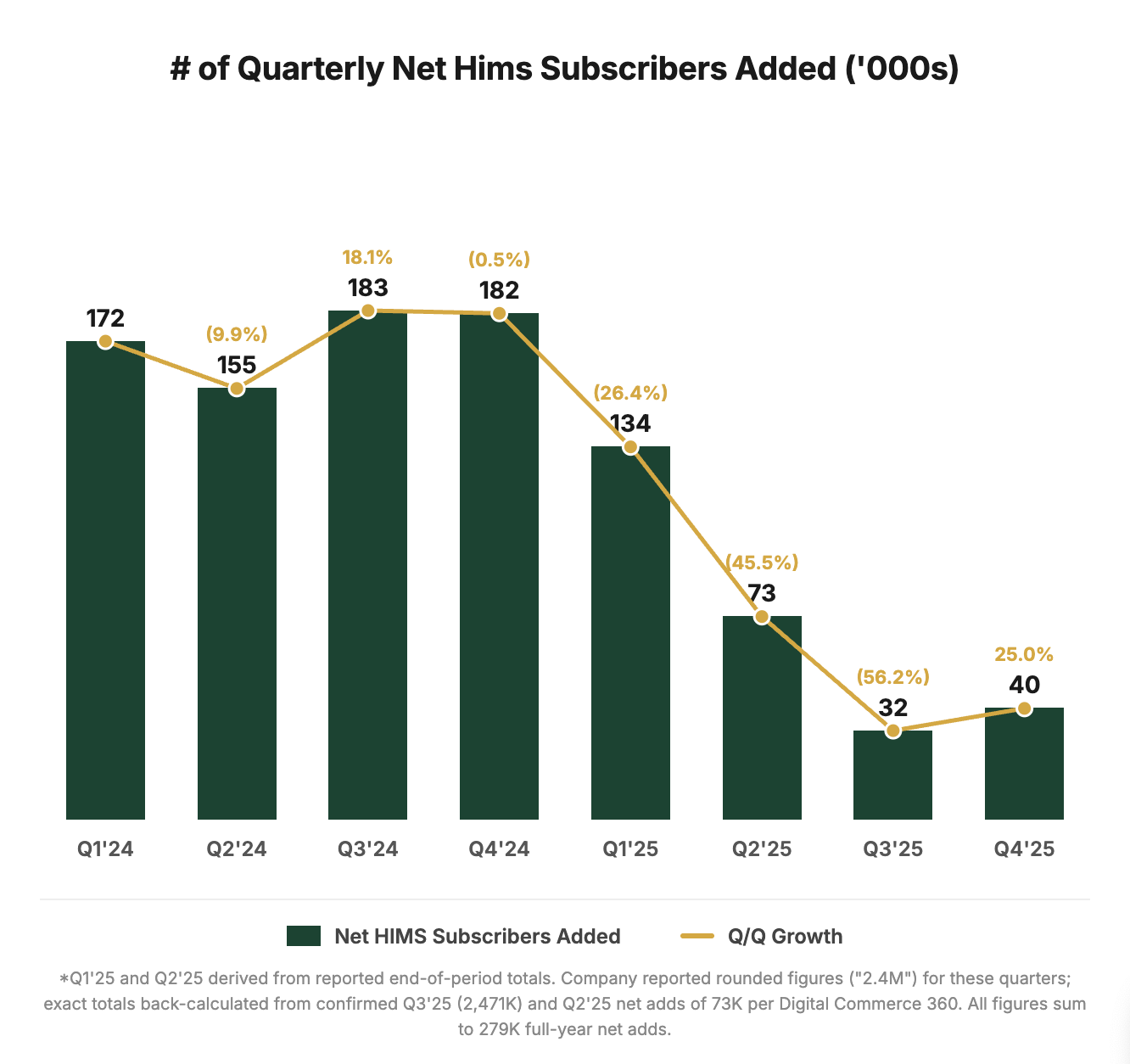

1. Adding subscribers is getting expensive

Over 2.5 million people are now subscribed to the Hims & Hers platform, which is a pretty insane figure when you consider that Cleveland Clinic, one of the largest and most famous hospital systems in the world, sees about 3.1 million unique patients a year.

But the problem is that the headline number is doing a lot of heavy lifting.

Hims added roughly 40,000 net new subscribers in Q4 2025. In the same quarter of 2024, that number was around 182,000, meaning a year-on-year deceleration of nearly 78%. That’s not something an investor wants to see from a hypergrowth company.

My first reaction to this was: woah, woah, what’s going on here? Is this just a growing business maturing? Netflix and Amazon both hit periods where subscriber growth slowed dramatically, and my instinct was maybe that this is just a natural part of scaling.